On Thursday evening, Strathcona Resources announced their intention to commence a take-over big to acquire MEG Energy (link to PR). This immediately followed the sale of their Montney assets on Wednesday evening, for ~$2.7Bn in cash and securities (link to PR). On the aggregate, Strathcona erased ostensibly all of their debt, while only selling ~20% of their field cashflow. Given their private equity roots, and focus on responsible employment of leverage, we had expected that Strathcona would bring their leverage back up to ~1.5x EBITDA in the coming quarters. It's clear that reintroduction of leverage is going to happen sooner than we expected.

You'll have to excuse our language — but Strathcona's offer, and the coinciding math — is a load of antagonistic horseshit. When adjusting the transaction metrics for MEG's turnaround, along with actual 2025e costs, one would uncover the deal is laughably dilutive for MEG shareholders. The Strathcona slides are a total farce, with a notes section that reads more like a standalone encyclopedia than an appendix. Not only can MEG improve their business much more on a standalone basis through 2030; than Strathcona can through 2030 — the change in governance, and strategies between both companies cannot be more different. But the point is moot. Modelling anything past 2026, with Strathcona in the fold is an erroneous exercise. Management will keep executing deals; making any long-term estimates futile. MEG shareholders need to know they are joining a completely different business as a minority shareholder; rather than continuing on their current, near bulletproof trajectory.

Strathcona's quickly timed bid for MEG is no coincidence — we believe that Strathcona sold their Montney for the sole purpose of funding a bid for MEG. In the first week of April, we received the marketing materials for "Project Bear Creek"; and just ~40 days later Strathcona announced the full sale of their Montney division. They moved quickly, raising money to allocate into oil sands assets that have been rocked YTD due to concerns over tariffs. Despite direct tariffs on Canadian crude exports not coming to pass; equities remained depressed due to global tariffs dampening demand growth forecasts. While we have circulated client notes discussing the long duration, and low maintenance nature of the underlying heavy oil businesses; the equities have been sluggish to recover. We expect that Strathcona, and the Waterous Energy Fund are moving in direct reaction to this mispricing.

Ultimately, we believe that Strathcona will be successful in their bid for MEG. We discuss the reasons why within. Central to our view, is the assumption that Strathcona wouldn't launch a bid they couldn't win. It was Adam Waterous that invented the game; so we don't expect him to lose playing it. We think that the Waterous ecosystem has more liquidity than the broader markets are currently underwriting; and that for Strathcona, MEG is an extremely strategic asset, as it allows them to rapidly consolidate the rest of the WCSB's independent heavy oil producers using immediately more desirable paper.

We expect that Strathcona will do everything they can to close MEG, as it allows them to be a much more compelling consolidator of the oil sands fairway. Strathcona needs MEG, badly. MEG’s asset is far more strategic to Strathcona, and the Waterous Energy Fund; than it is to any other potential acquirer. Cenovus, Suncor, CNRL – all can continue to execute their long-term strategy without MEG. Strathcona can’t. After closing their Montney dispositions; we originally expected that Strathcona would be very scrappy in adding barrels back into the portfolio. We assumed over the next 12 months, Strathcona would likely accumulate lower quality, but oil weighted resource. Though this timeline arguably makes more sense – and now we expect Strathcona will still accumulate lower quality resource; but after acquiring MEG. Having MEG derisks the quality part of Strathcona’s portfolio for future sellers, and makes their paper much more attractive for the lower quality acquisitions that we still expect to come (though, most assets are lower quality compared to MEG).

The Waterous Energy Fund’s strategy (and by extension, Strathcona’s strategy) is not one of modest annual growth, or small tuck-in acquisitions – it’s a strategy of rapid resource accumulation at a time when multiples are historically low, and leverage is almost non-existent. We believe that the Waterous family (proprietors of WEF, the majority owner of Strathcona), have the goal of buying, ostensibly, every independent secondary recovery heavy oil asset in the WCSB. We believe that Strathcona needs to close MEG, as it allows them to continue using their paper, and off-balance-sheet leverage via WEF, to take advantage of a period in the industry where; a) companies are notably under-levered; b) very cheap (compared to historical valuations); and c) M&A competition is almost entirely absent.

To do that, they’ll need credibility beyond what they already have. WEF and Strathcona already have a reputation of being extremely competent dealmakers. Adam Waterous, the co-founder of Waterous & Co. which was acquired by Scotiabank in 2005 to form Scotia Waterous; has no need to prove himself as M&A savvy. It’s widely recognized that he ran the best A&D shop in the industry for over a decade before leaving to start his current private equity fund (WEF) in 2017.

In fact, WEF’s reputation in town is only one of being good dealmakers. They have very little operational credibility; which is fair, given how poorly they have integrated some of their recent acquisitions (namely, Serafina). Strathcona needs a reputation for being a good operator, that’s backed by a high-quality asset base. MEG delivers just that. MEG is unanimously considered to be the best independent oil sands asset in Canada; and acquiring it immediately lends credence to Strathcona’s portfolio quality. Overnight they move from Tier 3, to Tier 2+. If we’re right, and Strathcona’s medium-term plan is to use their paper to anchor incremental deals while adding material leverage to continue acquiring assets – they need to be something that shareholders of target companies want to own. Adding MEG to their portfolio will help Strathcona’s quality standing considerably.

We don't think it's a coincidence they are launching this bid at a time when;

At this exact point-in-time, competition for MEG uniquely low, driven by preoccupied, or properly levered competitors. This is a unique moment where there is very little realistic competitive for such a high quality asset. We think Strathcona may have also orchestrated part of their competitors struggles. We think there is a very good chance that CNRL was not the highest bidder for Strathcona's Pipestone assets; but Strathcona elected to take CNRL's offer, in order to reduce their liquidity. Pro forma the Pipestone acquisition, CNRL's demand liquidity is ~$4.4Bn; with ND/FFO of ~1.1x currently, it wouldn't be overly easy for CNRL to come in over-the-top for MEG. They would have to push net debt to $25Bn (a pro forma ND/FFO multiple closer to 1.4-1.5x) to buy MEG on the balance sheet — so not comfortable, but CNRL could do it. But, we don't think CNRL will, as it greatly inhibits their ability to add resource elsewhere; it would be unlike CNRL to tie effectively all their liquidity up paying a premium for an asset as commodity prices are softening.

To make things even more interesting — we also think it's no coincidence that every single sell side institution in the city (save for Peters & Co., and TPH & Co.) were paid by Strathcona in some capacity, in conjunction with their recent Montney disposition. Strathcona knows that loyalty lies with money (in most cases).

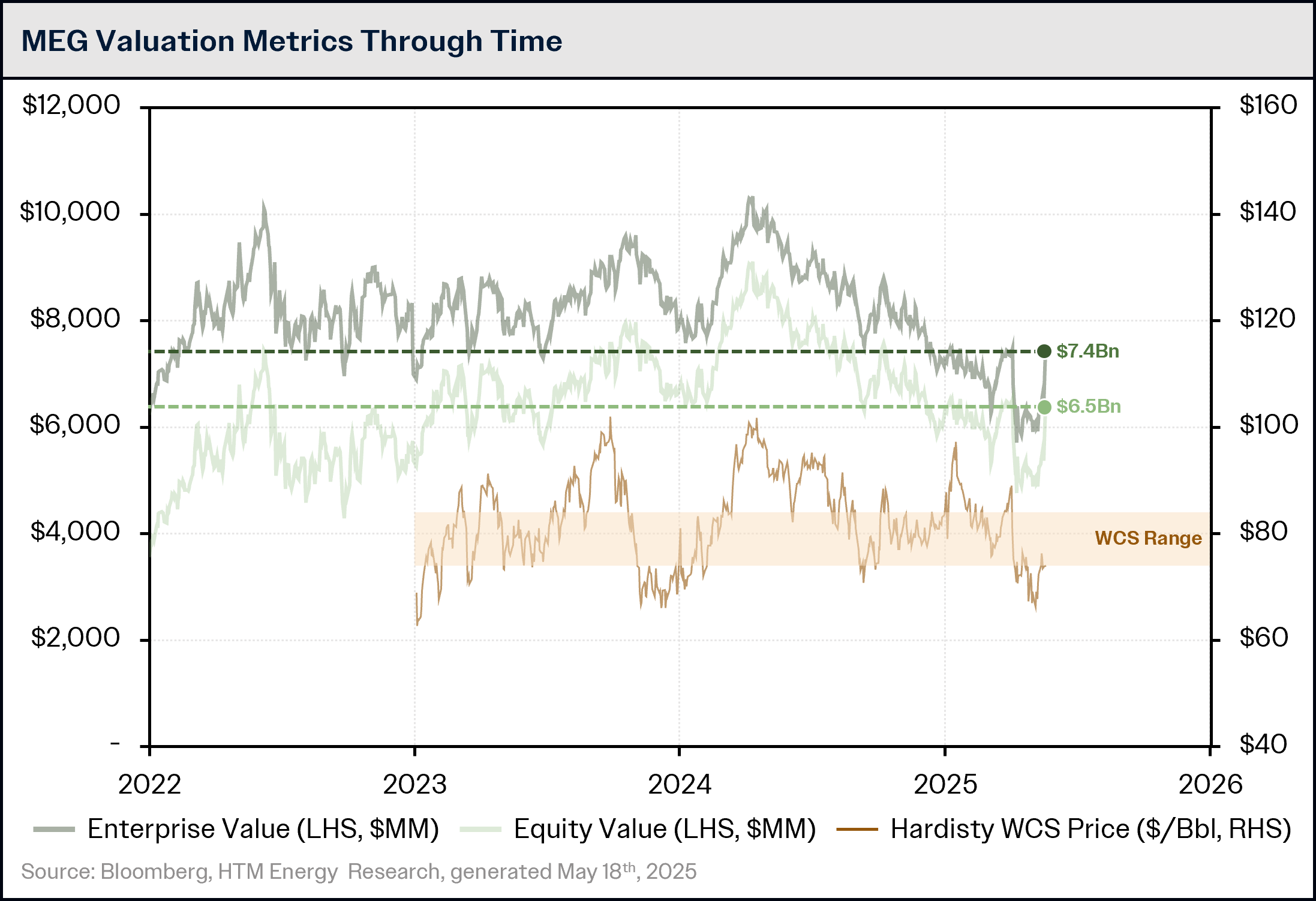

Strathcona has intentionally set themselves up — launching this process at a time when their peers are distracted or weak; and at a time when MEG's valuation is so disconnected from underlying fundamentals, that even a much more substantial premium than their initial 9.3%, would still be an arguably great acquisition price. As we've discussed in notes this year; MEG's valuation has adjusted such that they can both fund their major CAPEX program, and fund a full 10% NCIB at ~US$70/Bbl WTI. Despite MEG's stock trading up 20% on Friday, MEG's enterprise value is still at the low end of its 3-year range. Even at 30% bid premium for MEG's equity, after giving effect to their YTD buyback and debt progress (HTM estimates for both figures), the TEV would only be ~$7.9-8.0Bn which is in-line with their 3-year range. Not to mention that MEG has spent measurable CAPEX YTD on ordering long-lead items for their 30,000Bbl/d Christina Lake expansion project. So, we think that the timing of Strathcona's offer is no coincidence, as debt progress, buybacks, and growth haven't yet been priced into MEG's stock (in our view).

Presumably, this entire process by Strathcona was initiated in response to MEG's weak equity price; we don't think that Thursday's bid was simply opportunistic — it has been very well orchestrated, and we have to assume WEF is confident they have the wherewithal to close the deal. If they put MEG into play, but didn't have the ability to buy it, we think that the viability of Strathcona's medium-term strategy is greatly compromised, with quite literally not another opportunity to buy another asset of this quality and scale. We have to assume (and would suggest that clients generally assume), that Strathcona has manufactured their offer, and timeline; to keep them in a consistent position of strength throughout the chaos that will inevitably unfold over the next 2-4 months.

In fact, we don't just assume that Strathcona has timed this offer well — ae assume that Strathcona has ruthlessly calculated exactly how much Cenovus can pay (and also gamed out disposition scenarios), thus, they have to want Cenovus to bid. If Cenovus is the only other bidder, we believe that Strathcona thinks they will be able to defeat them at a shareholder vote (with an increased offer). Again, if Strathcona loses MEG, there is not another asset like it in the basin. Athabasca comes close, but it's ~1/3rd the size, and doesn't cement Strathcona in the top ranks of anything.

As it stands right now with Strathcona being the only offer; shareholders have 2 options; a) sell to Strathcona; or b) ignore Strathcona. If Cenovus bids, the options become; a) sell to Strathcona; or b) sell to Cenovus. We think that the Waterouses are counting on that happening — and think that their pure-play upstream story will be able to beat Cenovus' downstream integrated story — especially at a time when Cenovus' downstream performance has been optically very poor. Not to mention the recent blowout at Cenovus' Rush Lake SAGD project. Meanwhile, Strathcona just took down a huge win selling the Montney for a large gain on cost, and have boosted Tucker Lake's SAGD production to all-time-highs, nearing 30,000Bbls/d.

Ultimately, we expect the next few months to play out something like the timeline below. Cenovus will make a white knight bid after a Sunrise deal with Suncor (as Strathcona expects, taking Suncor out of the equation), after which Strathcona will increase their bid.

At this point in time, the heavy oil fairway — from the oil sands, to the Clearwater — is notably cheap. As we have discussed in recent publishings, the free cashflow breakeven on a maintenance basis for the SMID cap heavy oil E&Ps, is radically lower than those of US shale companies. Despite this; heavy oil assets, with RLI's that are often a full decade higher than their shale peers — trade in-line with the US shale E&Ps. Notably, the oil sands companies also lack any material leverage — making for a compelling situation if you're a private equity group OK with some debt...

Below we show an "acquisition value heatmap" — it's a sampling of forward growth, free cashflow, inventory life, and current relative leverage. The oil sands, and heavy oil fairway stands out as being a high-value target for deals. Companies are unlevered, with material inventory carry. While there are a handful of similarly compelling opportunities in the Montney and Duvernay; they are visually not as concentrated as the heavy oil fairway(s).

Breaking down the above heatmap even further; we show debt on the left, and 5yr HTMe TSR on the right. While there are numerous companies that have manageable leverage throughout the basin; there are 3 oil sands companies with cash on the balance sheet. This is extremely unique. Similarly, as shown on the right, there are a number of Montney and Duvernay companies with competitive 5yr TSRs, they often already have leverage, making them incrementally less attractive in an acquisition.

We believe that Strathcona has taken stock of the industry — and realized that a massive amount of resilient and high-quality heavy oil cashflow trades with effectively no leverage, and at a very high free cashflow yield (on a maintenance basis) — in some cases, a free cashflow yield so high, that just levering the company's own cashflow in-line with US shale peers would provide enough funding to acquire the entire company. It's a concert of low multiples, an industry-wide push to delever, tight WCS differentials, and tariff threats weighting on equity sentiment. For anyone with the ability to buy the business down here; they are going to be hugely successful over the long term — and that's where we think WEF/Strathcona is at.

Below we show an example of what it would have to buy 300,000BOE/d of production. Using the balance sheet/funds flow from the 3 companies with a net cash balance sheet, it would only take ~$5Bn of incremental funding to own the entire universe if levered to 3x FFO; and ~$10Bn if levered to 3x FFO while paying a 30% bid premium. Though, as we detail below; using FFO as a leverage target for these heavy oil type businsses distorts the lower maintenance requirement. If we were to assume 6x maintenance free cashflow (which is reasonable directly post-deal-close), to own the 300,000BOE/d peer group below, a buyer would only need ~$1.7Bn in funding to acquire it at market. These are wild statistics. Even with a 30% bid premium, the incremental funding is ~$6.4Bn.

When you compare Canadian leverage to US leverage, the difference is stark. Many names in the heavy oil fairway (Athabasca, Headwater & Spur), carry cash on their balance sheet; while also having a notably lower base decline rate than their US peers, owing to widespread implementation of secondary recovery in the cold flow fairway, and of course, SAGD in the Athabasca fairway. Many US E&Ps are now trading >6x levered on a free cashflow basis. What's notable though, is that the lower reinvestment rate required for heavy oil E&Ps, means that gross FFO leverage may look higher than it actually is. A number of US shale E&Ps are now levered >6x FCF, given the much higher maintenance capital requrements, as a percentage of cashflow, needed to maintain unconventional production. In our view, 6x maintenance FCF is an aggressive leverage target, but we don't think unreasonable by any means, especially compared to the US.

And why not? The gas producers execute something extremely similar — operating as a going concern even when gas prices are at rock bottom, and cashing it when prices infrequently spike. Oil cashflow is less volatile than gas (so more amenable to leverage), but Strathcona has also managed their differential exposure through the acquisition of a 250,000Bbl/d crude-by-rail terminal. While economics will never be as competitive as via pipeline, it's a massive-size option with effectively no premium.

With a strategy similar to this; Strathcona could feasibly consolidate, through public companies (shown on the map to the left), an in-situ oil sands portfolio that is equally as large as Suncor, and similar in size to CNRL. While Strathcona would lack mining — they claim that's a selling point. If Strathcona was to chase both publics and privates; their map would look something like the right, and they'd have a bigger SAGD portfolio than Suncor. Again, we reiterate that Strathcona's paper is materially more appealing to the private operators with MEG inside the company, than as a steady-state operation.

Within, we discuss why we believe Strathcona will aggressively pursue MEG. The banks that did publish comments on Friday suggested that a transaction price of ~$28/sh would be fair, if not likely. We, on the other hand, believe that any acquisition price below $30/sh is too low — and we detail why below. We have worked backwards, starting with an unlevered IRR target; and then backing into a share price — and ~$30-32/sh is where we end up. Below we show a probability distribution that represents our range of MEG price outcomes 3-4 months from today. Earlier in this note, we provided a rough timeline of how we expect events to unfold. Ultimately, we see ~20% further upside to where we think MEG will transact. To the downside; MEG is not as optically cheap as other oil sands peers, trading at a DAFCF multiple ~20% higher than peers (mostly motivated by Friday's price move), so we would expect a price ~$22/sh to be the downside anchor.

If we revisit our Tariff Trade Playbook; we really liked MEG at $20/sh, as there was very strong line-of-sight to generating a >15% IRR owning the equity; while retaining material upside to commodity price moves without seriously risking returns at ~US$60/Bbl WTI. Essentially, Strathcona is trying to internalize most of that at a time when the stock has been sold down, for really no reason. The underlying fundamentals of MEG's business are strong as ever, with almost no balance sheet leverage, and a project currently underway to add 25-30,000Bbls/d of bitumen production, for ~$700MM. If you think about that, MEG is going to grow by 25%, for a capital cost <10% of their enterprise value. Commodity prices aside (they are not at risk of insolvency), that is a phenomenal piece of business, and no reason Strathcona should be the beneficiary of the work that has gone into progressing Christina Lake's expansion project.

Recall our October 2024 Birchcliff note, where we ran a simulation to determine the PV10% of future FCFPS, when considering gas prices as randomized, rather than as fixed or using a forward strip. We executed a similar simulation, but this time considering MEG growing Christina Lake to 135,000Bbls/d of bitumen capacity, with WTI prices randomized between US$50/Bbl and US$110/Bbl. What we found, is that at $30/sh, there is still an extremely strong chance of an acquirer delivering an unlevered IRR of >12%, and at Friday's close of ~$26/sh, the odds of an >11% IRR are almost certain. In-fact, at $26/sh, an acquirer of MEG could, with reasonable confidence (>51%), deliver a >13.3% unlevered Atax IRR on the deal. Any tax treatment, and leverage could easily see that ratchet higher than 16%. For a Tier 1 asset with decades of inventory, we feel like a 16% IRR is too high. Under no circumstance do we think that MEG shareholders should let an acquiring party have a >50% chance of generating an 11% unlevered IRR. Ultimately, that maps to a ~$32-33/sh ceiling for the equity; but at the same time, a 11% unlevered IRR for a highly strategic asset, is still very respectable.

Given MEG's resilient free cashflow netbacks; between US$60/Bbl and US70/Bbl WTI, we expect acquiring MEG will deliver an ~8-11% IRR, on an unlevered basis. The left chart shows a share price and WTI sensitivity, while the right chart shows how synergy capture changes economics. Note, the chart on the right considers a WTI price of US$70/Bbl, and a long term WCS discount of -US$12/Bbl. Note, that moving synergy capture ~$50MM in either direction moves the IRR ~70bps. Important for two reasons; a) we don't believe Strathcona can truly deliver $175MM of synergies; and b) we're confident Cenovus can deliver >$150MM of synergies. This should move Cenovus' offer (that Strathcona will have to leapfrog) higher, and ultimately provides us confidence MEG will transact above $30/sh.

We will publish our full accretion/dilution model at a later date. The key takeaway, is, after fairly rigorous modelling, that on metrics we deem key, and adjusting 2025e numbers to be truly representative of the business — in no world is Strathcona's proposed deal accretive to MEG shareholders. MEG shareholders should demand more, much more, for Strathcona, or any other acquirer. When we drill into the numbers, only at a ~0.725x exchange ratio, and a $11/sh cash payment, does accretion for Strathcona shareholders become at risk. This is where we think that Strathcona is prepared to end up. Here (a $33/sh total consideration), the deal is still 2-3% accretive on a PPS basis for Strathcona shareholders, ~1% accretive on an Atax FFOPS basis, and ~6-8% accretive on an Atax maintenance FCFPS basis.

Forgetting the farcical figures published by Strathcona for a second — the numbers remain clear; with Strathcona's current offer, MEG shareholders are worse off combining with Strathcona. Not on an accretion/dilution basis; but simply considering where the business will be in 4-5 years.

Inside Strathcona's Q1 MD&A, they disclose an expanded credit facility of $3.245Bn, with an accordion feature that would allow that facility to expand to $3.545Bn. Strathcona's current debt capital structure includes $720MM of senior notes and facilities totalling $2.2Bn. Assuming Strathcona doesn't touch their senior notes, their current liquidity maps to ~$4Bn immediately following the closing of their Montney dispositions.

Note the dates — in Strathcona's MD&A, they disclose "on [Friday] April 25, 2025, the availability under the Revolving Credit Facility was increased to $3.0Bn"; then subsequently, in their initial MEG bid intention release, Strathcona discloses "On [Monday] April 28, 2025, Strathcona made a formal written combination proposal to the board of directors of MEG, with the same consideration as [this] offer". This implies that Strathcona's original offer was made with no premium, at ~$20.20/sh worth of total consideration. Strathcona's stock is up ~18% since; representing an offer ~14% better.

This is a pathetic offer — and again, we have to believe that Strathcona, and the Waterous Energy Fund fully knows and acknowledges this.

The expansion of their facility is notable — as Strathcona has a history of immediately drawing almost their entire facility just months after its expanded. We have reconstructed Strathcona's historical liquidity picture through obtained filings, and previous disclosures.

Strathcona runs their facility draw hot, averaging ~75% drawn outside of the price windfall of 2022 (which they promptly plowed into Serafina). Using 75% facility draw as a target would imply that Strathcona is looking to level their pro forma net debt out at ~$3.4Bn attributable to Strathcona. This, plus the ~$4.7Bn equity part of their offer, maps to an ~$8.1Bn TEV, os a ~$29/sh transaction consideration. But — recall that MEG has a ~$1.2Bn facility (entirely undrawn); drawing this at 75% pro forma would imply a $900MM contribution, bringing their potential offer to a TEV ~$8.9Bn, or ~$31-32/sh. Mapping very closely to our IRR simulation figures.

Note, that WEF III has committed to acquire 21.4MM shares of Strathcona, adding ~$650MM to Strathcona's treasury. This moves ~$650MM from WEF III LPs, into Strathcona, and provides WEF III with margin-able securities (Strathcona common stock). We expect that WEF will continue to commit to deals on a pro rata basis; essentially equitizing would-be debt. We assume this structure will serve two purposes; a) to derisk Strathcona's balance sheet; but also b) to make sure that WEF can carefully manage accretion/dilution, which will in effect cap upside for the minority shareholders. This is a complicated, and potential very gross governance (and capital) structure. Ultimately, we think that the Waterous ecosystem liquidity picture is underestimated. We think that the Waterouses, through WEF, and Strathcona, have ~$6.5Bn in liquidity. Including the implied $4.7Bn stock portion of Strathcona's offer; this would imply the ability to pay up to ~$11Bn for MEG (though if they would transact at that price remains questionable).

Ultimately, the fact that WEF is backing into the MEG deal via sub receipts should signal to Strathcona shareholders that WEF III will actively monitor (and weasel away) accretion from Strathcona shareholders. Though, we'd note this is speculation, and we're unsure of capital at risk limits within the WEF III structure.

But, it's essentially getting more of what we already have, which is long life, low decline, high free cash flow oil [production]. And when we think about the business that we're building, the business will be what we believe is going to be the only investment grade long life, low decline, high free cash flow oil company that does not have mines or refineries in North America. — Adam Waterous, Q1 call

We thought Strathcona/WEF would approach the consolidation of oil sands assets the other way around — buying all the smaller projects first; then acquiring the big independent producers (Athabasca and MEG); though clearly they believe adding MEG first makes for a more compelling proposal when they inevitably propose to acquire the projects shown below (i.e. the remaining SAGD SMIDs, and private independents).

We have understood that Strathcona/WEF asked one bank to underwrite $6Bn in notes. This suggests to us, that Strathcona (plus WEF), is willing to materially increase the cash portion of their offer — but also, that they a dead-set on getting MEG as a portfolio anchor for their future acquisitions.

So it's abundantly obvious to us, that Strathcona (and by extension, the Waterous Energy Fund), wants to continue to accumulate all of the independent heavy oil assets in the SAGD fairway — to ultimately position themselves as the largest independent low-decline oil producer that doesn't have a refining arm. And likely not just SAGD producers; eventually we imagine this will include the heavy oil producers that have great waterflood, and polymer flood projects, though we imagine that Strathcona will give the independent Clearwater/Mannville producers more time to organically progress polymer and waterflood expansions.

We appreciate this vision; even buy into it — though they are grossly undervaluing MEG given they offer nothing strategic or incremental for MEG shareholders.

If Strathcona was successful in this; they'd be one of the top bitumen producers in the Country, with a portfolio that would be genuinely meaningful to global supply.

When married with Strathcona, the governance structure changes materially, and for the worse for MEG shareholders. The Waterous Energy Fund; through their pro rata subscription, and ownership in Strathcona, will control 51% of the voting common stock of Strathcona. We do not expect they will relinquish that control in any scenario.

We like MEG because of their no-nonsense, predictable execution. We cannot say the same for the Strathcona team; who are (extremely clearly) very unpredictable. The beauty of MEG is that it’s a low risk steady state business trading at a low multiple. Strathcona is the opposite.

Similarly, Strathcona's board is hilariously poorly aligned with the common stockholders. Of the 9 board members, 7 of them work for, or have worked for Strathcona, or the Waterous Energy Fund. None of the Strathcona board has any operational experience, which we deem to be extremely important.

MEG shareholder will transition to being led by a very capable team, with a good governance structure — to being effectively minority shareholders in a firm controlled by bankers with ostensibly no operational experience. That is a major downgrade for MEG shareholders. While we think that an M&A-focused firm can certainly add a lot of value in Canada, where the velocity of transaction capital is meaningfully lower compared to the US; we don't think MEG shareholders should want to be a part of that, for such a paltry premium.

Athabasca's stock was right to be +9% on Friday. Ultimately, we see Athabasca as an acquisition target in the future. We think there is a chance that MEG seeks to block a Strathcona hostile bid, through a friendly merger with Athabasca. If Strathcona is successful acquiring MEG, we would expect that Athabasca would be their next target. We still maintain that Athabasca has line-of-sight to ~$12/sh by the early 2030s. We imagine that the best defence for the industry will be to simply ignore Strathcona — though that would require collusion from multiple integrated E&Ps, which would in-turn break a litany of anti-competition laws. Alternatively to defend, MEG and Athabasca could merge, which we are not writing off.

Suncor needs to nail the Rich Kruger follow-through, and fix their upgrader problem in the next few years to fully earn the "repaired" stamp of approval. The root of Suncor's issue isn't the mine life at Base Plant; it's letting their upgrader run out of bitumen. Suncor can replace mined bitumen with bitumen produced in-situ (i.e. SAGD). The most strategic asset in the mix is Sunrise, which is currently owned by Cenovus, and directly offsetting Suncor's existing Firebag SAGD project. Sunrise has 6.7BnBbls of bitumen in place, and we deem ~4BnBbls of that as technically recoverable. At Cenovus' current target production rate of 60,000Bbls/d, Sunrise has a productive life of >150 years.

MEG would be an odd transaction for Suncor. Sure, Suncor needs bitumen, but there is no physical integration with Suncor's current footprint and MEG Christina Lake. MEG would be a corporate transaction that could be beneficial; but it doesn't necessarily solve the problems they have at Base Mine (resource life, and the regulatory inability to expand the mine footprint). Suncor's Base Mine is >100km away from MEG's Christina Lake project. For Suncor, getting Sunrise from Cenovus almost fully solves their upgrader/Base Mine problem, and allows them to backfill Base Mine with in-situ production — so we think that's what Suncor will try to get done, rather than chase MEG.

Below we show a local map of the greater Fort McMurray oil sands area. Suncor Firebag, and Cenovus Sunrise are practically already integrated. MEG could be accretive, but it's not strategic; and we think sends the wrong signal — that Suncor is simply pressing their cost of capital advantage, rather than being calculated. Recall how badly Advantage fumbled when they simply did a deal because they could last year, instead of being deliberate and tactical with their capital deployment.

Below we show a satellite map of Suncor, and Syncrude's surface mining operations. Suncor has applied to expand their Base Mine to the southwest, but this comes with a rigorous, and impossibly lengthy regulatory process that could quite literally, last the better part of the next decae. Getting Sunrise has the potential to both be accretive to production, while solving short-term anxiety over the upgrader feed — and if their Base Mine expansion is approved, Suncor has the optionality to grow Sunrise independently, or maintain it as a free cashflow generation asset.

Cenovus is the obvious owner for MEG – but their capital markets sentiment has been challenged due to their downstream weakness. If Cenovus wants MEG, we believe they can move parts of their portfolio around to accommodate such. Namely, move Sunrise into Suncor (solving problems for Suncor), and the Deep Basin into Tourmaline (a deal we think Tourmaline would do, and we discuss below). We think that Cenovus can raise $5.5Bn for Sunrise, and $3.0Bn for the Deep Basin. This would provide Cenovus with the cash to close MEG with no incremental equity (providing them with a much stronger bid than Strathcona's equity/cash mix); but would also deliver +35,000Bbls/d of oil production, while being minority positive to cashflow. We believe that Cenovus has a much better ability to actually drive synergies at Christina Lake, given the almost perfect overlap with MEG's assets.

Recall, 2024 through 2028, we estimate that Cenovus will spend $5.1Bn to organically grow 150,000BOE/d (Cenovus’ guidance of $5.3Bn of capital, 160,000BOE/d of growth). 75,000BOE/d of that total is in-situ growth. Through 2030, Cenovus has ~$3Bn of debt due; which is <0.5x HTMe 2026 FFO. There is room on Cenovus’ balance sheet to add MEG to their portfolio, in concert with other dispositions. While MEG would not compete directly with organic opportunities they are currently pursuing; Cenovus has the best odds of driving material synergies on the property.

Cenovus could take MEG onto the balance sheet if they really wanted to — but certainly to the chagrin of shareholders. While we agree that operating efficiency could be improved; the continued negative FFO contribution has been more driven by the macro environment (i.e. NYH diesel cracks falling from US$65/Bbl in 2022, to US$25/Bbl in 2024), rather than entirely Cenovus’ controllable performance. Granted, their US refining market capture has been exceptionally weak in 2024. We expect, that later this year, when the bickering between Cenovus and Strathcona becomes public — events like Cenovus' Rush Lake blowout, and their poor 2024 downstream performance will be pressed by Strathcona, to encourage MEG shareholders to side with them.

We think there is a good chance that Tourmaline will see an opportunity to offer Cenovus cash for their Deep Basin complex. Thus, the potential impact on Tourmaline could be very positive. We believe that Tourmaline would be willing to pay, and under the right circumstances, Cenovus would be willing to accept; ~$2.85-$3.15Bn for the entire Deep Basin complex. This represents ~6x asset-level FFO, with Tourmaline having the ability to materially grow the asset, while also improve the cost structure (we model Cenovus' Deep Basin as having per-unit operating costs ~55% higher than Tourmaline). While Tourmaline has recently said they don't want to engage with deals >$1Bn (and we note that Advantage is also potentially on the market); we think that Tourmaline would be able to pay cash for the entire Deep Basin package, a valuable consideration for Cenovus. Tourmaline is really, the only potential acquirer for this asset, and certainly the only one that could close fast, and pay cash. Net of Topaz equity, Tourmaline's pro forma leverage would be <1x 2025e FFO, with line-of-sight to reduce that to <0.8x in 12 months, and ~0.6x in 12 month if modelling a Topaz infrastructure drop-down.

When Cenovus acquired most of ConocoPhillips’ Canadian assets in 2017, the Deep Basin produced 120,000BOE/d, and Cenovus had the plan to grow that to >150,000BOE/d by 2020. Today their Deep Basin complex produces ~95,000BOE/d. Despite having a massive infrastructure footprint, and a highly desirable NGTL transport portfolio; Cenovus has kept the Deep Basin undercapitalized for almost a decade, despite pockets of good well results. Cenovus has run an extremely high-graded capital program year after year; without meaningful delineation throughout the ~850,000 acre Chinook Ridge field. Cenovus planned to drill >100 Deep Basin wells annually when they announced the acquisition, but since, they’ve averaged just 30 annual TILs. While Cenovus clearly likes the Deep Basin part of their business (and we note they have potentially been adding Sinclair area Montney acreage via Crown Land sales); we think they’d far rather have incremental oil sands production, than the Deep Basin.

We have to assume that Tourmaline knows, and appreciates that Cenovus would want to engage with MEG — and will make a cash offer for Cenovus' gas assets. For Tourmaline, Cenovus’ Deep Basin makes sense; it’s ~5,500 gross sections (3.5MM acres) of under-exploited gas resource with a very low PDP decline. Recall that Tourmaline sees the Deep Basin as effectively "one large gas field”, and Tourmaline’s position in the play would effectively double overnight, to almost 7MM gross acres of leasehold after acquiring Cenovus' position. Cenovus’ Deep Basin also comes with 1.4Bcf/d of processing capacity, including ~0.8Bcf/d in the Chinook Ridge/Kakwa area; where Tourmaline has been delivering extremely strong drilling results.

Cenovus’ Deep Basin has been notably undercapitalized, with almost no drilling in the Chinook Ridge area, and close to no activity in the Greater Edson/Sundance area either. Cenovus has a large BC Deep Basin position where the gas travels into Alberta; which advances Tourmaline’s goal of having BC-facing gas optionality. Cenovus has focused on channel sands in the Sundance area (i.e. Notikewin), but hasn't attempted to drill any shoreface plays; aside from the Falher at Wapiti. Below we show modern horizontal and deviated Deep Basin wells — there hasn't been much activity across Cenovus' lands. Note, while there has been significant commingled vertical production at Chinook Ridge, for the most part, that is localized to a Cadomin field straddling the border; with tighter sands untouched.

We see serious upside in the Falher around the AB/BC border at Sinclair, and in the Dunvegan at Wapiti/Elmworth. Over the past 2 years, Tourmaline has continued to test horizontal wells in areas where vertical wells encountered hydrocarbons, but the sands were too tight to produce – typically offsetting prolific gas pools. This has been a continued successful endeavour – their most recent Belly River horizontal saw an oil peak IP30PD rate of ~700Bbls/d. Vertical offsets saw peak IP30 rates of 20-40Bbls/d of oil. We think there’s massive potential for this to be successful throughout Chinook Ridge – though Cenovus has not allocated the capital required to truly tame the asset. We think Tourmaline can (and would want to); especially given the infrastructure ownership – key to Tourmaline’s ethos.

Provide your email below and we will send you a complimentary basin activity report every quarter.

© HTM Energy 2025

Calgary, Alberta