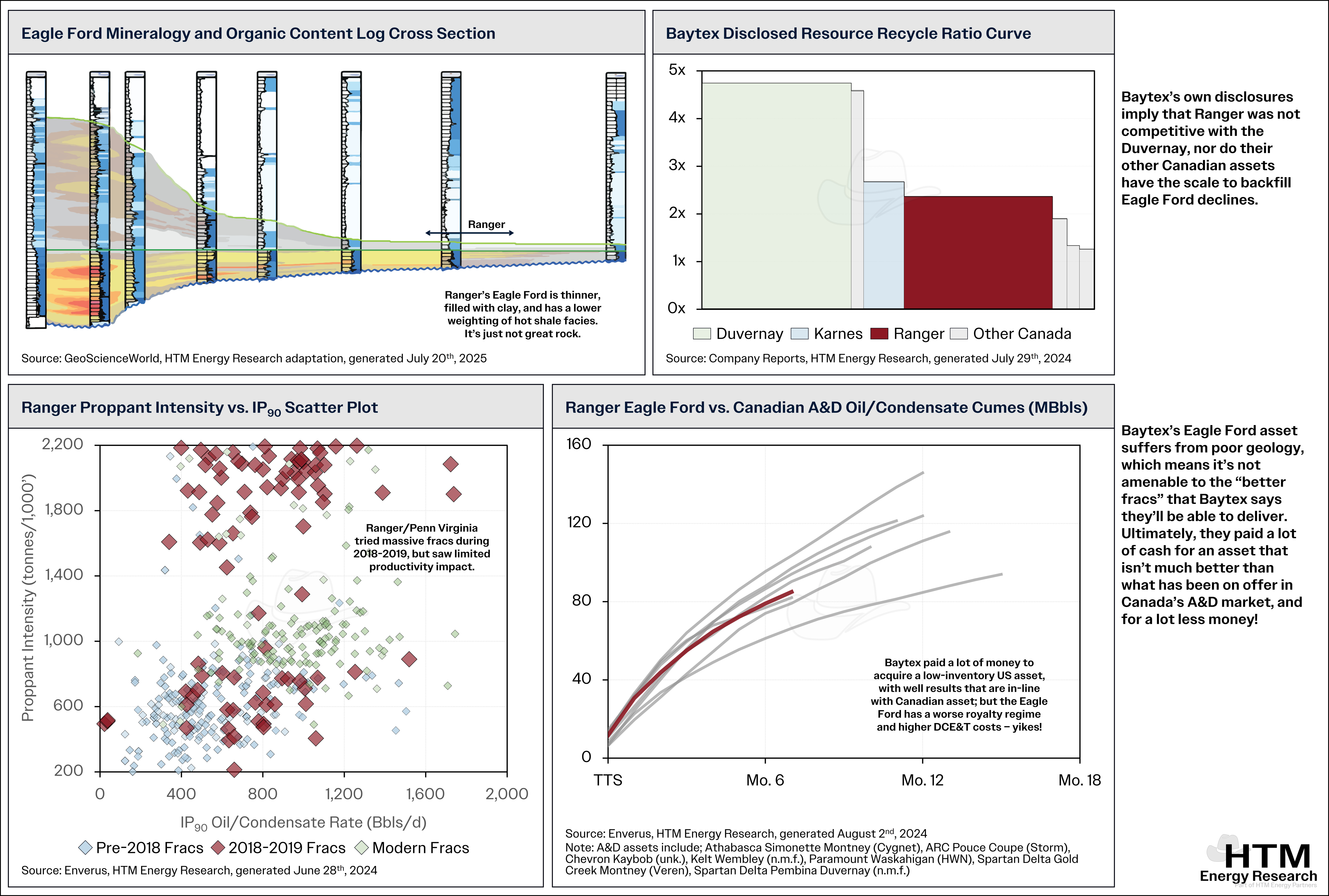

In 2023, Baytex acquired Ranger Oil, expanding their position in the Eagle Ford. This will likely go down as one of the worst deals of this oil-price-cycle. Baytex’s acquired Eagle Ford assets are seeing (and will continue to see) productivity degradation, and ultimately the acquisition added an erroneous business unit (note, Baytex didn’t have a Houston office before Ranger) that nobody wanted and didn’t truly solve any problems. Ultimately, the root of Baytex’s problems are they’ve done nothing to make themselves desirable, they don’t satisfy any themes in the market, and have failed to be a first mover in the Duvernay. Ranger diluted the positive aspects of their legacy business, to the point where new organic growth from the heavy oil unit, or Duvernay, will be so greatly overshadowed by the Ranger acquisition – that healing the business is impossible. Thus, we have a pointedly negative outlook on Baytex, given their very low-quality geology that will not respond well to their stated plans to “frac the Eagle Ford better”, with limited ability to grow, and broadly incoherent strategy.

Baytex has tried to build scale over the years, but they’ve always bought low-quality assets near the top of the cycle; this time is unlikely any different. A lack of grounding within the organization contributes to inconsistent strategy and execution. Certain anchor assets in Baytex’s Canadian portfolio (Lloydminster, and the Viking) are largely sub-scale and also facing downwards pressure on EURs, or just low-quality all-around. Lloydminster heavy oil wells will never backfill the monstrous declines they inherited in the Eagle Ford. At Peavine, they’ve overcapitalized the play, having grown mostly using Tier 1 inventory which is depleting fast. Inventory life becomes a real concern at Peavine within 3-4 years with conventional pay quality degrading fairly rapidly moving outwards from the initial development area.

In the Eagle Ford, Baytex was exit liquidity, with Juniper having stripped the good condensate acreage out of the Ranger package prior to selling. Baytex’s assets lie in an area of higher clay content (less amenable to bigger fracs), and they are deep, so more expensive to drill and complete (moving south). Their new wells have been underperforming their own budgeted type curve which will manifest as rapid deterioration in free cashflow margins. Despite their claims, Baytex has less than 10-years of inventory in the Eagle Ford, and that’s including refracs, which haven’t been successful.

Baytex should have consolidated the Duvernay. They had the ability to, but it wasn’t via a marketed package (Ranger was). It would have been more work and more risk; though they would have earned credit as a resource developer – but added immense value in the process. Baytex has a very good Duvernay position they inherited in their acquisition of Raging River. Instead, Baytex has muddied their business, adding capital inefficient Eagle Ford shale with no inventory to grow that will see downwards pressure on EURs (instead of upwards pressure, like the Duvernay would have offered). We think that Baytex has material downside to their true underlying value, with the large air gap mostly motivated by their gross over-pay for Ranger’s Eagle Ford assets.

We include an overview of our position in a video-format below.

Provide your email below and we will send you our public previews when released.

© HTM Partners 2025

Calgary, Alberta