Whitecap has shown the way in terms of building a durable company, equipped with ample Tier 1 inventory; and doing so while prudently managing leverage. Whitecap has increased simple production per share over 2-fold since inception. Today Whitecap trades at a lower pre-Veren-deal enterprise value than it did in 2021, with 60% more production. Whitecap is a leading Canadian E&P, and we think is a must-own going forward. Today, it’s priced extremely attractively. Whitecap and Veren have formed what we believe to be the best positioned company in the basin. Full stop. This was a sector-defining transaction that has created a senior E&P – and the market isn’t pricing it anywhere close to that. Whitecap is a must own equity, and now, by far, our highest conviction long-term idea in the unconventional play trends (along with Spartan). Whitecap is offering a well covered 9-10% dividend yield – which implies a payback on purchase today, before tax, of ~10 years. In 10-years, we see Whitecap as producing well over 500,000BOE/d, with ~15 years of supporting inventory. The mix of cash yield, plus growth/inventory carry is extremely compelling.

We were extremely excited about both individual companies, and think at their pro forma size, will be impossible to ignore when they hit their stride in 2026. We continue to think the market has misclassified Whitecap as a boring and potentially undisciplined acquirer delivering low-single-digits growth. In reality, we think Whitecap will post high-single-digits annual growth consistently over the next 4-6 years, with almost 40% cumulative growth through 2030. Recall, on their conference call, we asked if they’ll continue the same growth that each individual company had planned to deliver – their answer was largely “yes”. We don’t think people appreciate how much growth Whitecap’s pro forma asset base can support. We calculate that just 115 sections at Lator can support 80-90,000BOE/d of growth and maintenance for >10 years. While Whitecap doesn’t plan to reach that plateau until 2032, it’s significant that just one of their pro forma projects, which is largely derisked with an infrastructure partner in place; represents 20-25% corporate growth. Pro forma Whitecap has over 1,600 gross Montney sections, and 800 Duvernay sections. We expect Whitecap to clarify their growth plans in the coming months – though clients should appreciate just how much they can deliver today.

Needless to say, we’re incessantly excited about Whitecap pro forma, and have to imagine the street, and broader market will catch up in the coming quarters/years. Using mid-cycle commodity prices, we think Whitecap has an organic growth runway to >600,000BOE/d, with a solid cache of locations that breakeven <US$40/Bbl WTI on the oil side, and <$0.50/Mcf on the gas side. All the reasons we were excited about Veren and Whitecap as independent issuers, persist with more intensity as a combined entity. Our independent work would echo an achievable ~$150MM in annual synergies. Our project build-up below sees further upside to miscible flooding in Saskatchewan along with upside from continued M&A, which we expect. In-fact, we think Whitecap has a 12-18-month window to continue their M&A follow-through, with Kiwetinohk, and potentially Strathcona (Montney) – all while ARC seems hesitant to transact in lieu of delivering a “down the fairway” year. A handful of manageable transactions, well within the realm of possibility, would solidify Whitecap as not “a” dominant – rather “the” dominant, unconventional Canadian E&P.

The pro forma company moves two E&Ps, each on the cusp of operational scale; into decidedly large-cap territory. And it’s lonely up there, with ARC the only liquids-rich peer outside of the oil sands having both operating scale, and resource of scale. While there are plenty of E&Ps with good, high quality unconventional inventory – there are few that have operational scale like the pro forma Whitecap does. While “scale” is a term that can get thrown around loosely – and something that many companies claim to have, Whitecap now truly has “scale”, with the key ability to compartmentalize operations to maximize efficiency while sporting a newfound buying power. A good example of this is the fact that combined Whitecap/Veren are running 10 rigs in the Montney and Duvernay right now. Just level-loading their rig pace would reduce their rig demand down from 8-12 intermittently, to 7-9 year-round. We think this can amount to ~$20-25MM in CAPEX savings annually. In comparison to US peers, the combined company now has a ‘core’ inventory footprint better than leading Permian operators on both an absolute, and relative basis. For example, Permian Resources only has 1,000-1,200 core locations, we see Whitecap with over 2,000. This inventory footprint, and operational scale will be hard to overlook as positive quarters and well results continue to populate.

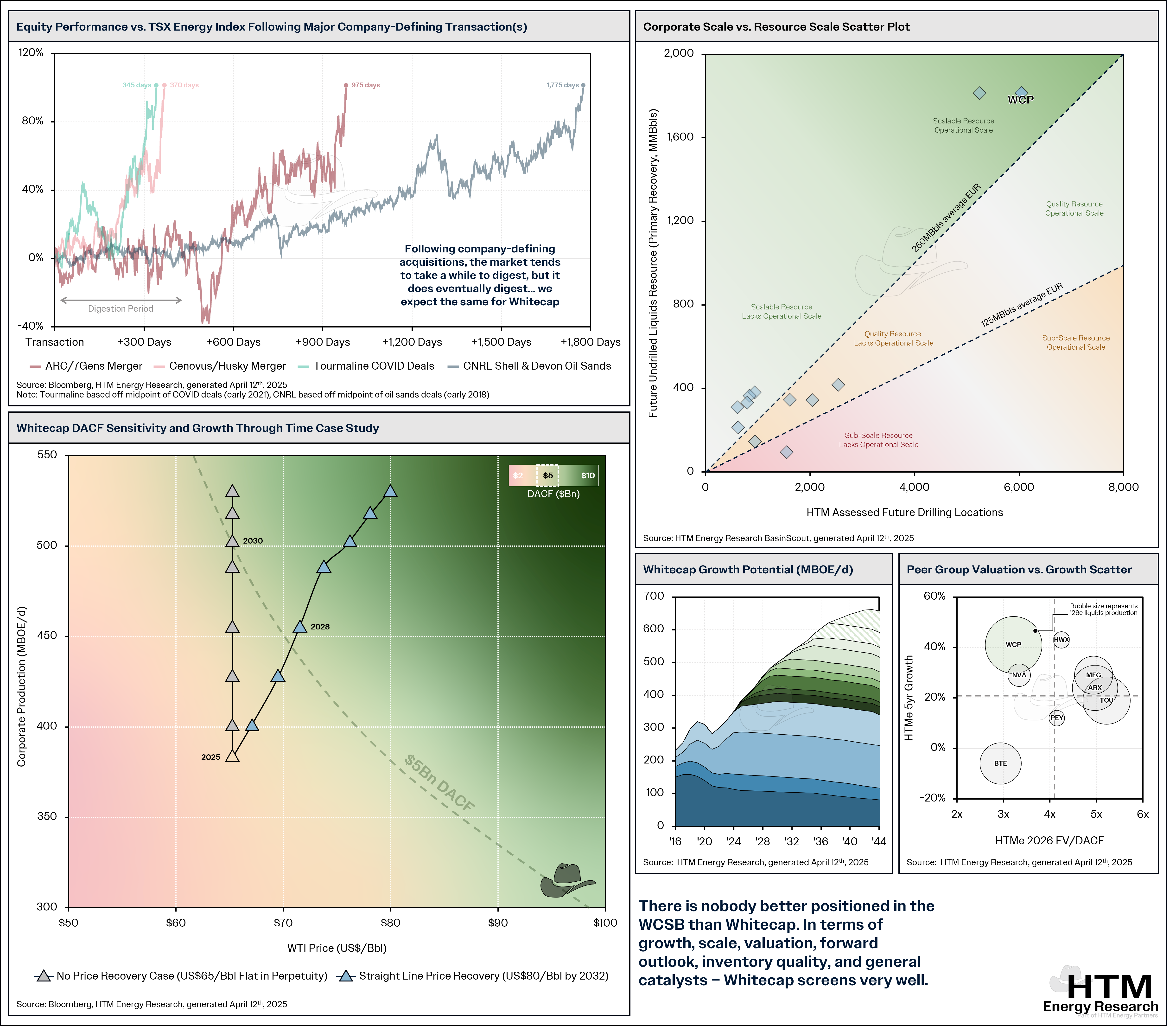

All deals in Canada that have solidified the acquiring party as a “major E&P”, has led to the acquirer's equity delivering +100% outperformance over the energy index in the years following the transaction. We believe this merger with Veren is remarkably similar to ARC’s merger with Seven Gens in 2021, which brought together two companies similar in size to Veren and Whitecap. As ARC delivered steady execution and growth, the eventually rerated higher. We’ve already watched Whitecap execute extremely well after acquiring XTO, which gives us confidence in their ability to keep delivering consistent results in the Montney and Duvernay.

We think Whitecap can deliver similar returns. From here +100% would imply an EV of $22.5Bn, at 4.5x EV/DACF, this maps to $5Bn in DACF, which we view as easily attainable within 3-5 years without any improvement in oil prices (i.e. US$65/Bbl flat WTI). Below, we show a “path to $5Bn in DACF” sensitivity. We think this is achievable within their current asset base – while also noting that Whitecap will likely continue with M&A, as they have done successfully since inception.

There are near-infinite permutations of growth, and price scenarios that would get Whitecap to $5Bn in DACF. Some include M&A, many are price driven, similarly, many are growth driven. Though we are confident that Whitecap can achieve $5Bn in DACF (consistently, not just at peak prices), within the next 3-5 years. We expect Whitecap can do this without adding any incremental risk into the business (i.e. overindulging leverage).

Once Whitecap crosses $5Bn in DACF, we see their total payout ratio as being ~70% (including the dividend), which is extremely manageable, and maps to a ~10-12% FCF yield. and why we think Whitecap, like ARC, will work to get their all-in payout ratio down over time by growing their top-line volumes. We see this as a near-term priority for Whitecap, with their next tranche of growth from Lator, where we assess their stated plateau at 80-90,000BOE/d as entirely achievable, and backed by low-risk acreage. Lator is extremely impactful liquids-rich inventory that competes with the best in the Montney and Duvernay. As Whitecap continues to dispatch projects like this over the coming decade, we believe the market will have no choice but to slowly appreciate how well Whitecap has positioned their business since COVID.

Provide your email below and we will send you our public previews when released.

© HTM Partners 2025

Calgary, Alberta